In March the incumbent UK Government announced a slew of new gas-fired power plants to deliver spinning reserve to cover the GB grid for those windless winter days with no sunshine.

At the time, Energy Secretary Claire Coutinho said: ‘There are no two ways about it. Without gas backing up renewables, we face the genuine prospect of blackouts… There are no easy solutions in energy, only trade-offs… As we continue to move towards clean energy, we must be realistic.’

On the face of it, the argument appears sound, however evidence would strongly suggest otherwise.

With increasing penetration of cheap renewables onto the grid, the cost of marginal gas generation will become increasingly expensive and will drag up consumer bills.

This is a genuine paradox – more cheap renewables equals higher electricity bills – and is an unfortunate consequence as we advance intermittent green power across a grid system originally designed for dispatchable power sources utilising coal, gas, nuclear and hydro.

As Coutinho says, trade-offs are required – but if we want consumers to truly benefit from the cheapest forms of electricity (i.e. renewables), and to get fully on board with net zero, then some new approaches are required.

Renewables are cheap

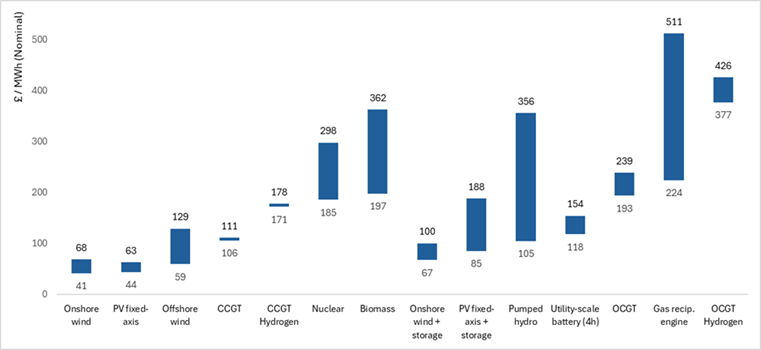

No one can now dispute that renewables are cheaper than fossil fuel generation as evidenced by the graph below with the LCOE of different technologies – and we now see capacity additions outstripping their fossil fuelled equivalents globally.

By 2025 renewables is on track to overtake coal as the largest source of global electricity generation.

The UK is in the vanguard. In 2023, renewables supplied 47 percent of the country’s power, up from just two percent in 1991. Low carbon nuclear power supplied 13 percent, while the remainder was fulfilled by gas suppling 31 percent, coal circa 1 percent, and 7 percent imported via inter-connectors from the continent.

However, despite the increasing penetration of low-cost renewables, over the last five years the UK socket price for domestic electricity has risen at a compound average growth rate of 12.8 percent.

Here’s why.

In the UK system, non-fuelled power generation from wind and solar have short run marginal costs close to zero and as such will always under-cut fuelled systems in the merit order system (i.e. cheapest power is dispatched first).

This is all well and good when there is plenty of wind and sun – but if there’s not enough to go round, then our spinning reserve gas plant has to fill the balance. This then sets the price for all electricity delivered in that half hour period.

Over the last five years, gas delivered at the National Balancing Point (NBP) – the virtual trading point for UK natural gas – has increased from 34.4p/therm to 76.0p/therm delivering a compound annual growth rate (CAGR) of 17.2 percent. At the point of use over the same period gas prices have a compound average growth rate of 16.4 percent while electricity is up 12.8 percent.

The balancing mechanism cost shown to right of the above chart is also playing an increasing role inflating electricity costs to the consumer. The UK’s National Grid, the electricity system operator, is tasked with constantly balancing supply and demand for electricity on the grid. It operates in real-time, meaning adjustments are made throughout the day to ensure a stable flow of electricity.

However, as a result of an increasing share of low-cost intermittent renewables displacing gas to power, there is now greater risk in matching supply with demand. In the event where forecast demand is not matched by generation, National Grid will make a call for power via the balancing mechanism at a premium price (due to lower utilisation – see ‘Balancing Act’ section below) from dispatchable sources which are largely made up from carbon emitting gas fed power generators and the heavily subsidised, inefficient Drax biomass plant (circa £800 million per annum).

These balancing mechanism costs were £2.9 billion in 2023 (compared with £4.2billion in 2022 which can be directly linked to the gas price spike post Russian invasion of Ukraine). The combination of balancing mechanism costs plus constraint payments due to insufficient grid infrastructure are equal to £139 for an average electricity bill payer, representing 11 percent of the annual consumer electricity bill in 2023. (compared with 14.5 percent in 2022).

It is therefore no coincidence the marginal price setter of gas to power in the merit order has a strong influence in the cost of delivered electricity in the UK.

Consumer Utility Costs

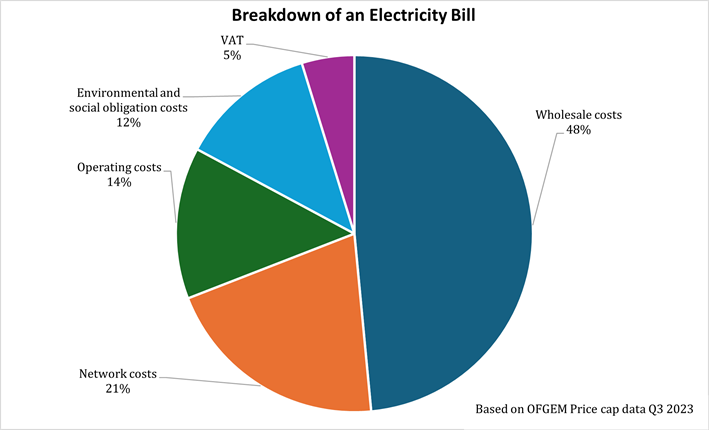

To evidence the cost of electricity to the consumer we have provided a breakdown based on Ofgem data from Q3 2023. Electricity bills are built up from a number of components which vary over time impacted by economic activity (demand for power), inflation, infrastructure spend (e.g. grid upgrades) and commodity price movements from gas to power. The four main elements which make up an electricity bill are:

- Wholesale costs (48 percent) to generate power.

- Grid costs (21 percent) covering transmission, distribution and balancing costs.

- Environmental and social obligations (12 percent) which includes net subsidies to renewables.

- Operating costs (14 percent) are retail energy supplier margins.

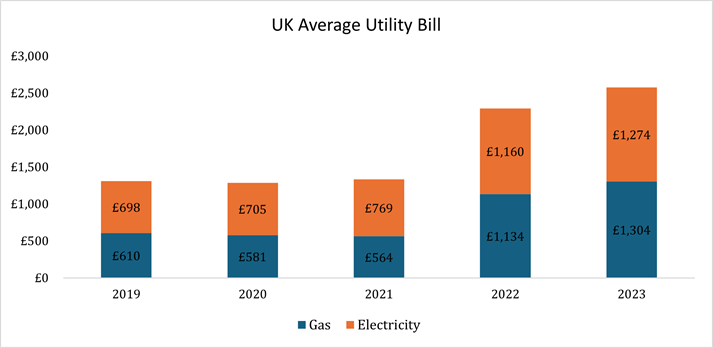

In the bar chart below we provide data from the UK Government Department for Energy Security & Net Zero (DESNZ) demonstrating the impact gas to power pricing feeding through into the retail utility bills as the marginal price setter combined with increased gas heating costs shown in blue.

The spike of 2022 was a consequence of the Russian invasion of Ukraine with the panicked switch from piped gas to LNG resulting in abnormal wholesale and balancing systems costs.

The commodity price spike from gas to power led to UK government intervention through the introduction the energy price cap to keep a lid on overall consumer bills. Despite this intervention around 28 energy suppliers collapsed with the liability (£2.7bn) socialised across bill paying consumers.

Balancing act

As renewables take increasing market share in the UK, there will be economic consequences to keep existing and new gas generators online to stabilise the grid as well as provide backup in periods of low wind and solar resources.

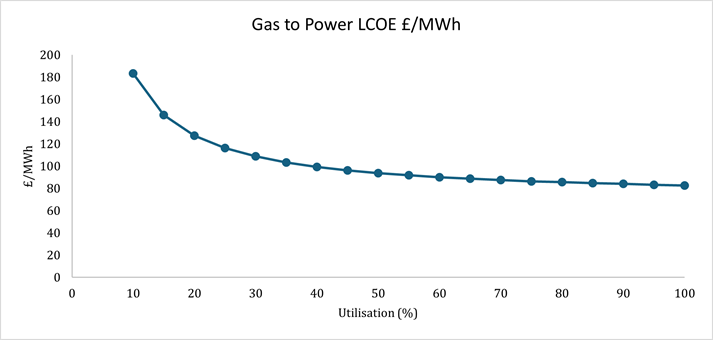

Although balancing costs fell in 2023 as gas prices fell, future gas turbines will be required to deliver less primary power and only balancing. This means that not only will the requirements for balancing rise, but the balancing market will have to bear the capital cost of turbines, driving prices much higher.

This problem will only increase as renewables take more market share. As gas to power capacity utilisation shrinks the cost of balancing the grid commensurately rises.

In the following table we show the impact of reducing gas to power utilisation – leading to increased capacity payments to these generators combined with the last unit of demand being fulfilled by the most expensive power delivered.

Source: Gneiss Energy modelling assuming 8.5 percent owner IRR (unlevered), NBP prices indexed, capex opex numbers from BNEF.

Aurora Energy Research estimates that unabated gas fired back-up capacity of 5GW will be needed, at a cost of £5 billion – putting an average of £178 on each household’s annual energy bill for a decade.

These costs will only increase when gas-fired generators are required to capture and store their carbon.

In reference to Coutinho’s comments about the need for back-up power from gas, this should be put into context with renewable energy resources across Europe. Mereological data confirms periods of little to no energy generated by wind and solar is commonly known as dunkelflauten. Across Northern Europe these events occur on average between two to ten times a year, or between 50 and 150 hours on average per month during the peak winter months of November, December, and January (3.4 percent annually).

There are sufficient back up sources from waste biomass and biomethane to support these periods combined with increasing pumped storage, hydro and untapping 11GWs of predictable tidal power within the UK.

Labours plans involve not only the creation of a new UK energy company to crowd-in the private market but to also move the net zero grid to 2030. Ed Miliband is keen to use as many tools at his disposal to drive grid decarbonisation which will likely mean increased allocations under the CfD mechanism which will no doubt involve ramping up predicable dispatch from the likes of hydro, pumped storage and tidal.

So, although UK Energy Secretary Claire Coutinho was right to say that trade-offs are required, is building an expensive new gas fleet, which will only increase bills, the best way forward?

It won’t be a surprise that redoubling our efforts to make our grid fit for a net zero future will be key. But it’s not only on the power generation side – in tandem we need a much clearer national strategy to stimulate grid digitisation and demand side management solutions which will enable the drive to electric heating.

Technology at our disposal includes:

- Increase the size of the grid system, providing capacity to transport large volumes of renewable power from a lowest cost location (e.g. highest wind speeds, highest solar irradiance).

- Digitise the grid and infrastructure between low and high voltage connection points plus end users.

- Demand management – turn up demand and turn down to compensate for variable power from renewables.

- Bi-directional grid capability – a must for vehicle to grid (near zero marginal cost) and roof top solar.

- Heat batteries to time-shift demand and decarbonise hard-to-abate gas fired heating.

- Energy efficiency and insulation.

Demand management and bi-directional power conditioning equipment will be key to removing the need for three phase signal power from fossil fed thermal power plants which would allow for a greater share of renewables on the grid instep with greater grid utilisation.

If we want a decarbonised and fully electrified energy system, the technology is at our disposal to remove the need for an expensive balancing mechanism and back-up power supported by mass burn of wood chips and gas fed power generators.

If we manage this, we can deliver a renewables-dominated grid which can displace higher cost unabated/abated gas and become the low-cost marginal price setter – delivering lower prices at the socket.

If we don’t, we’ll not solve the paradox of low-cost renewables resulting in higher prices for consumers – and will fail to convince voters that net zero is a price worth paying.